Entry-Level Buyers Finally Catch a Break on Inventory

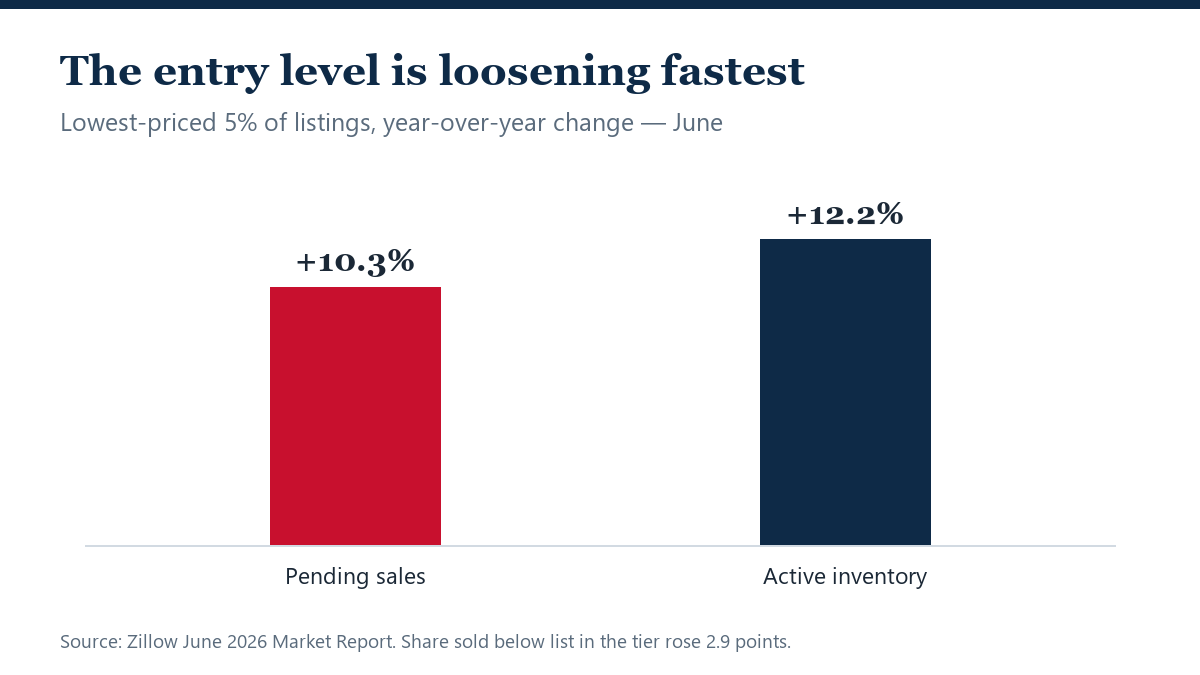

Pending sales in the cheapest 5% of listings rose 10.3% as inventory grew 12.2% — the entry level is loosening faster than the market at large.

Pending sales in the cheapest 5% of listings rose 10.3% as inventory grew 12.2% — the entry level is loosening faster than the market at large.

Wire fraud can drain closing funds in minutes. A verification checklist for buyers, sellers and agents before any money moves.

Short sales and foreclosures both involve mortgage distress, but the process, credit impact and buyer risks differ sharply.

Pre-foreclosure is the window before a foreclosure sale when homeowners still have options — and buyers face real risks.

Property taxes are squeezing homeowners hardest in 2026 where assessments lag prices. Where bills are rising the most.

Climate risk now belongs in home-buying due diligence. The flood, wildfire, wind and insurance questions to ask before closing.

Buying in a flood zone changes insurance, financing and resale math. A due-diligence checklist before making an offer.

Homeowners insurance is the missing line in most affordability math. Why coverage costs now shape what buyers can afford.

Homeowners insurance nonrenewals are rising as insurers reassess risk. What a nonrenewal notice means and what to do next.

Standard homeowners insurance usually excludes flood damage. What separate flood coverage does — and who actually needs it.

Debt-to-income ratio can make or break a mortgage application. How lenders calculate DTI and the limits that matter in 2026.

Mortgage applications are running above year-ago levels. What weekly application data says about buyer demand in 2026.

FHA and VA loans both help buyers with lower upfront costs, but eligibility, mortgage insurance and funding fees differ.

FHA and conventional loans help different buyers. Compare down payments, mortgage insurance, credit flexibility and loan limits.

Adjustable-rate mortgages can offer lower initial rates, but buyers need to understand caps, resets, margins and payment risk.

A 15-year mortgage can save interest and build equity faster, while a 30-year mortgage offers lower monthly payments.

A mortgage rate lock can protect buyers from rising rates before closing. Here’s when locking or floating may make sense.

Before signing a new-construction contract, buyers should ask about deposits, financing, warranties, changes, delays and inspections.

Spec homes are move-in-ready or nearly finished builder homes. Here’s why builders may discount completed inventory.

New-home supply and resale supply are sending different signals in 2026. Here’s why buyers see two different housing markets.

Housing starts fell in May 2026. Here’s why construction pullbacks matter for future housing supply, buyers, builders and prices.

Builder incentives can lower costs, but buyers need to compare rate buydowns, closing credits, upgrades and total price carefully.

New construction may offer incentives, while existing homes may offer better locations. Here’s how buyers should compare both in 2026.

Earnest money shows sellers a buyer is serious, but buyers can risk losing it if they miss deadlines or break contract terms.

Closing costs can surprise buyers and sellers. Learn what closing costs include, who pays them and how to review them.

An appraisal gap happens when the appraised value is lower than the purchase price. Here’s what buyers and sellers should know.

A practical home inspection checklist for 2026 buyers, including roof, foundation, HVAC, plumbing, electrical and safety issues.

Buying vs. renting in 2026 depends on location, time horizon, mortgage rates, rent levels and ownership costs.

How much are buyers putting down in 2026? Down payments fell to a four-year low, but cash still matters.

Seller concessions and price cuts solve different problems. Here’s when each strategy may help sellers attract buyers in 2026.

Get expert insights, market updates, and new opportunities delivered to your inbox.