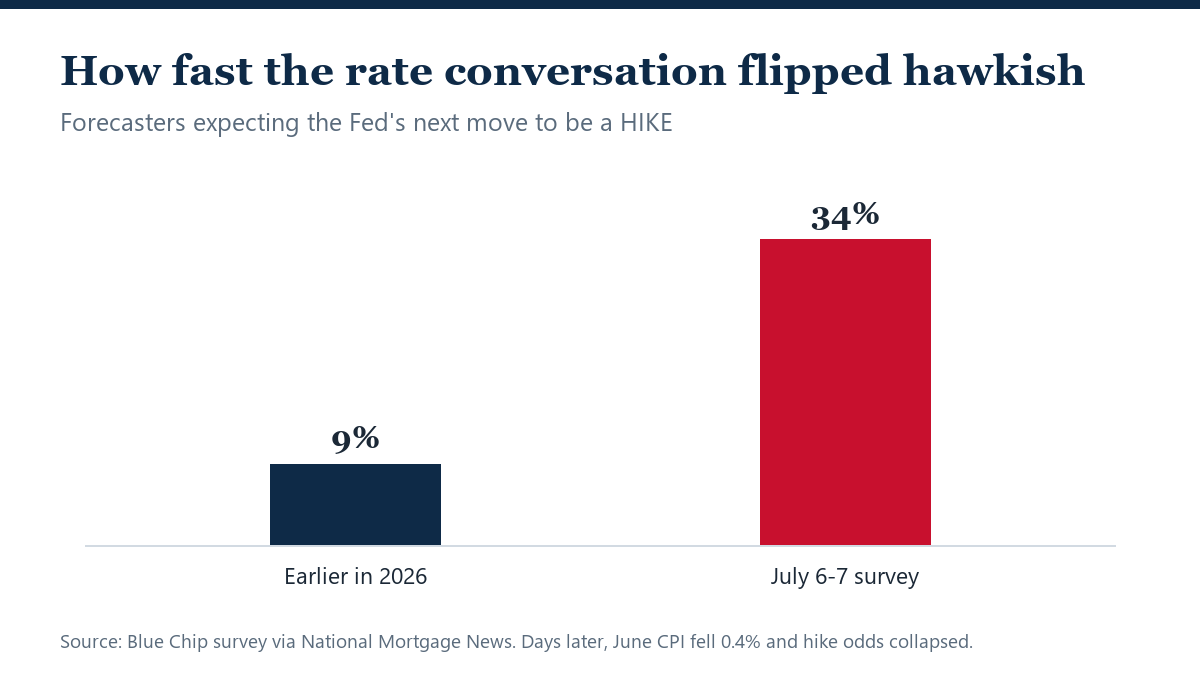

Mortgage Rates Hit 6.81%, Highest Level in a Year, as Applications Fall 2.9%

The MBA’s weekly survey shows the 30-year fixed rate climbed to 6.81%, its highest level in over a year, as overall mortgage application volume fell 2.9% in the week following the Fed’s July policy meeting.