Mortgage rates remain one of the biggest forces shaping the 2026 housing market.

Freddie Mac reported the average 30-year fixed mortgage rate at 6.47% as of June 18, 2026. The average 15-year fixed rate was 5.81%. Those rates are lower than some recent highs, but still high enough to keep affordability tight for many buyers.

The Federal Reserve also left its benchmark policy range unchanged in June. But homebuyers should not assume that a Fed pause automatically means mortgage rates will fall. Mortgage rates are influenced by bond markets, inflation expectations, Treasury yields, lender pricing and investor demand for mortgage-backed securities.

For buyers and sellers, the practical issue is simple: even small rate changes can move monthly payments enough to affect budgets, offers and negotiations.

Key takeaways

- Freddie Mac reported a 6.47% average 30-year fixed mortgage rate as of June 18, 2026.

- The 15-year fixed-rate average was 5.81%.

- The Federal Reserve held the federal funds target range at 3.5% to 3.75% on June 17.

- Mortgage rates do not move one-for-one with the Fed’s policy rate.

- Fannie Mae’s June forecast showed a 6.3% annual average 30-year fixed mortgage rate forecast for 2026.

- Buyers should compare payments at several rate levels before making an offer.

- Sellers should understand how higher rates affect buyer budgets and concession requests.

Where mortgage rates stand now

As of June 18, 2026, Freddie Mac’s Primary Mortgage Market Survey showed the average 30-year fixed mortgage rate at 6.47%. The average 15-year fixed rate was 5.81%.

For homebuyers, that means affordability is still the central challenge. A 6%-plus mortgage rate can significantly reduce buying power compared with a lower-rate environment, especially when home prices, insurance costs, property taxes and HOA dues are also elevated.

A national average is only a starting point. The rate a borrower is offered may depend on credit score, down payment, loan type, loan size, property type, points, lender, location and rate-lock timing.

Why the Fed does not directly set mortgage rates

Many consumers assume the Federal Reserve controls mortgage rates directly. It does not.

The Fed sets a short-term policy rate. A 30-year mortgage is a long-term consumer loan, and its rate is shaped by several market forces. These include inflation expectations, longer-term Treasury yields, demand for mortgage-backed securities, lender margins and the perceived risk of the loan.

That is why mortgage rates can rise or fall even when the Fed does nothing at a meeting. Bond markets often move ahead of the Fed, based on what investors expect inflation, growth and future policy to look like.

In June 2026, the Federal Open Market Committee decided to maintain the target range for the federal funds rate at 3.5% to 3.75%. The Fed also said inflation remained elevated relative to its 2% goal.

For mortgage borrowers, the key point is that a Fed pause is not the same thing as lower mortgage rates.

What Fannie Mae’s forecast suggests

Fannie Mae’s June 2026 housing forecast showed an annual average 30-year fixed mortgage rate forecast of 6.3% for 2026.

That forecast does not guarantee where mortgage rates will go. Fannie Mae’s own materials caution that forecasts are based on assumptions and can change. But the forecast does suggest that, as of June, a rapid drop far below 6% was not the base case.

That matters for both buyers and sellers.

Buyers waiting for much lower rates may get some relief if the market moves their way, but there is no certainty. Sellers may need to understand that many buyers are making decisions based on today’s payment reality, not on the hope of cheaper financing later.

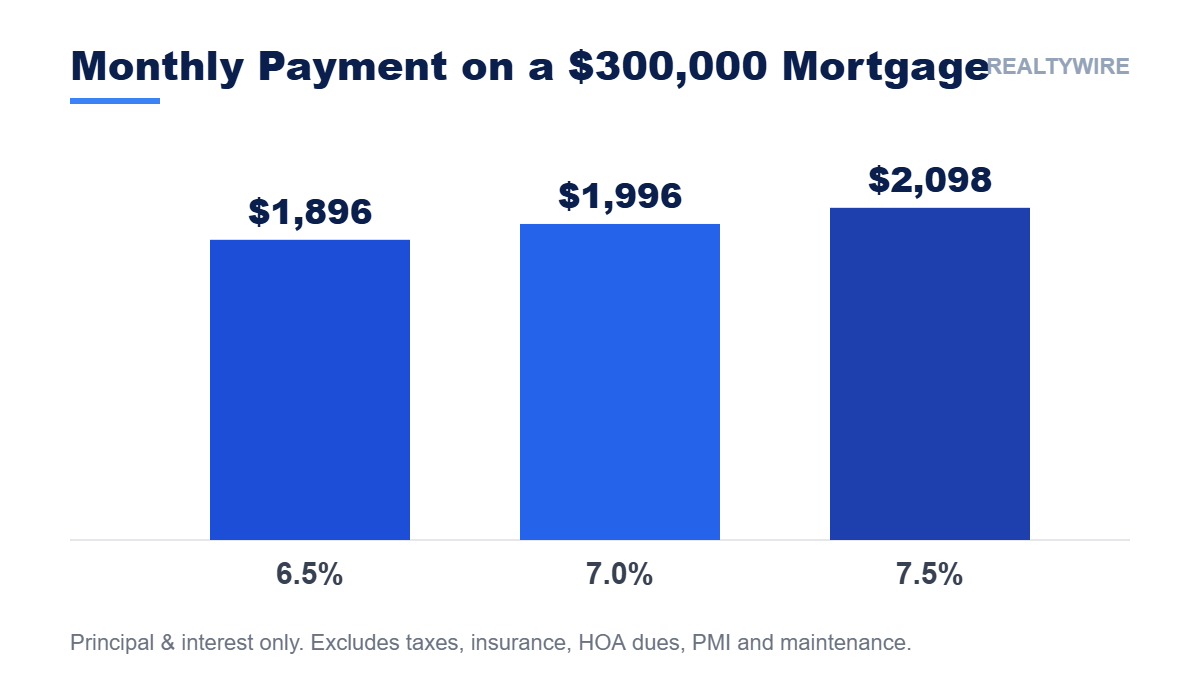

Payment examples: why small rate moves matter

Small rate changes can have a large effect on monthly payments.

Using a $300,000 mortgage example, approximate principal-and-interest payments are:

| Rate | Approximate monthly principal and interest |

|---|---|

| 6.5% | $1,896 |

| 7.0% | $1,996 |

| 7.5% | $2,098 |

These examples exclude taxes, insurance, HOA dues, PMI, maintenance and utilities. That distinction is important. In many markets, the non-mortgage costs of ownership can add hundreds or even thousands of dollars to the monthly housing cost.

Buyers should ask lenders to show payment scenarios at the quoted rate, 0.25 percentage points higher and 0.50 percentage points higher. That makes it easier to understand how sensitive the budget is to rate movement before making an offer.

What buyers should do now

In a rate-sensitive market, buyers should focus on total cost, not just the headline rate.

A practical checklist includes:

- update mortgage preapproval before serious house hunting,

- ask how long the rate lock lasts,

- compare payments at multiple rate levels,

- ask whether points, lender credits or temporary buydowns make sense,

- calculate taxes, insurance, HOA dues and PMI,

- compare resale homes against builder incentives,

- and avoid assuming that refinancing will be easy or immediate.

A lower rate can help, but it does not fix every affordability problem. A buyer still needs to understand the full monthly cost of the home.

What this means for sellers

Mortgage rates also affect sellers.

When rates are above 6%, buyers are often more payment-sensitive. That can lead to tougher negotiations, requests for seller credits, rate buydown discussions or lower offers.

Sellers should ask their agent how the monthly payment on their listing compares with competing homes. A $10,000 price adjustment, a closing-cost credit or a rate buydown can have different effects depending on the buyer, loan type and local market.

The best strategy is market-specific. In some cases, a price adjustment may be more effective. In others, a targeted credit may help a buyer overcome upfront cash or payment pressure.

Florida, Naples and seasonal-owner angle

In Florida and other second-home markets, mortgage rates are only one part of the affordability story.

Some luxury and seasonal buyers may pay cash or use large down payments, which can reduce the direct effect of mortgage rates. But financing still matters for many move-up buyers, investors and jumbo-loan borrowers.

Florida buyers also need to account for homeowners insurance, flood insurance where applicable, condo fees, HOA dues, taxes and possible special assessments. Those costs can change the real monthly payment even when the mortgage rate is the same.

For Naples and other coastal markets, the best analysis is property-specific. A lower purchase price may not be the better deal if carrying costs are much higher.

What to watch next

The most important mortgage signals to watch are:

- Freddie Mac’s weekly mortgage-rate survey,

- Federal Reserve policy statements,

- inflation data,

- Treasury yield movements,

- mortgage application activity,

- purchase-application trends,

- and builder or seller incentives tied to financing.

Fannie Mae’s Purchase Application-Level Index showed purchase-application dollar volume up 16.5% year over year for the week ending June 19, even though week-over-week activity fell during the holiday-shortened week. That mixed signal fits the broader market: buyers are still active, but affordability pressure remains.

Frequently asked questions

Why are mortgage rates still above 6%?

Mortgage rates are influenced by inflation expectations, Treasury yields, mortgage-backed securities, lender pricing and broader economic conditions. The Fed matters, but it does not directly set 30-year mortgage rates.

Did the Fed raise or cut rates in June 2026?

No. The Federal Reserve held the federal funds target range at 3.5% to 3.75% at its June 17, 2026 meeting.

Will mortgage rates fall below 6% in 2026?

No forecast can guarantee that. Fannie Mae’s June 2026 forecast showed an annual average 30-year fixed mortgage rate forecast of 6.3% for 2026, suggesting rates were expected to remain above 6% on average.

How much does a small rate change affect payment?

It depends on the loan amount and loan terms. On a $300,000 mortgage example, the principal-and-interest payment rises from about $1,896 at 6.5% to about $1,996 at 7.0%.

Should I lock my mortgage rate now?

That depends on your loan terms, closing timeline and risk tolerance. Ask your lender how long the lock lasts, whether a float-down option exists and what happens if closing is delayed. This article is general information, not individualized mortgage advice.

Sources

Freddie Mac Primary Mortgage Market Survey; Federal Reserve June 17, 2026 FOMC statement; Fannie Mae June 2026 Housing Forecast; Fannie Mae Weekly Mortgage Applications Data.